Bangladesh Economy 1990-2002

Compiled from a conference proceeding.

The Government of Bangladesh has been making vigorous efforts to accelerate sustainable growth for alleviating poverty and pursuing a strategy of private sector-led growth in a liberalized market economy. Bangladesh has undertaken extensive liberalization of the economy. The average tariff rate has been reduced from over 85% in 1992 to about 15% in 2002-2003. The maximum tariff rate has been reduced from 300% to 32.5% only, while all non-tariff barriers have been removed. The tariff regime in Bangladesh is the lowest in South Asia. Large-scale reform programmes in financial sector, legal system, administration, industrial, export & import policies, fiscal system, investment deregulation, etc. have been implemented and are underway.

As a result, some notable signs of progress in the economy, though moderate, are discernible. The growth rate of GDP which was averaging at 4.8% over two decades and in 2002-2003 the rate increased to 5.3%. GDP growth is expected to increase 5.7% in 2004 due to global pick-up, steady growth of Agriculture, exports and expansionary budget (ADB). It is also expected that GDP growth may be 7% due to PRSP.

As per new index of macro-indicators the level of investment has increased from 16.90% in 1990-91 to 23.2% of GDP in 2002-2003. The increase is mainly due to rising private sector investment as the public sector investment remained, more or less, stagnant. Domestic savings is low at about 18.23% of GDP mainly because of low-income base. As regards structure of the economy, agriculture remains the dominant sector contributing 18.23% of GDP. The manufacturing sector continues to remain small accounting for about 15.91% of GDP. The services sector expanded rapidly contributing about half of the GDP. There has been remarkable progress in the export sector with significant structural change. Merchandise export increased from 1.7 billion US$ in 1990-91 to 6.55 billion US$ in 2002-2003. The share of non-traditional exports accounted for 95.1% of total export earnings in 2000-2001 against 54% in 1989-90. About 95% of the total export earnings is contributed by the private sector. Exports, however, remain less diversified being dependent upon a few items, like ready-made garments, knitwear, frozen food and shrimps, etc.

Some improvements in the consumption of basic inputs have also taken place. Consumption of per capita electricity increased from 46 kwh in 1985 to 81 kwh in 1998. Energy consumption is however the lowest in South Asia. The per capita consumption of non-renewable energy in Bangladesh is 64 kg of oil equivalent as against 123 kg in Sri Lanka, 236 kg in India and 267 kg in Pakistan. The availability of telephone increased from 0.18 per 100 people in 1985 to 0.39 in 1997 against the world average of 10 per one hundred people.

In the context of fast changing global economic environment, liberalization of the economy is no doubt inescapable. But liberalization in our economy has been too much and too soon, compared to what our trading partners in South Asia have done. Consequently, foreign goods flooded our market and thousands of domestic industries have become non-performing. Industrial enterprises need time and facilities to make adjustments in terms of improving quality, increasing productivity, upgrading technology, modernizing equipment, etc. In this context Bangladesh needs to develop regional cooperation in trade and industry. Many countries have achieved commendable progress taking benefit of regional cooperation. The success of regional cooperation basically depends on policymakers of the governments, trade and industry circles, development agencies, professional bodies, academia and the people. All these factors will have to be pulled together for successful creation of a regional bloc. Now I would like to high light the trade position between Bangladesh and other countries including BMEST-EC countries.

Balance of Trade

Although imbalance is characteristic of Bangladesh’s trade. The trade gap is gradually increasing since 1996. However, Export earnings can at present meet import bills in higher proportions than before.

Export as a percentage of Import

| FY | Export | Import | Balance of Trade | Export as percentage of Import |

| 1972-1973 | 348 | 851 | (-) 447 | 43.95% |

| 1975-1976 | 380 | 1317 | (-) 937 | 28.85% |

| 1980-1981 | 710 | 2282 | (-) 1572 | 31.11% |

| 1985-1986 | 819 | 2120 | (-) 1301 | 38.63% |

| 1990-1991 | 1718 | 3511 | (-) 1793 | 48.93% |

| 1995-1996 | 3882 | 6827 | (-) 2945 | 56.86% |

| 1997-1998 | 5161 | 7545 | (-) 2384 | 68.40% |

| 1998-1999 | 5312 | 8005 | (-) 2694 | 66.35% |

| 1999-2000 | 5752 | 8403 | (-) 2650 | 66.45% |

| 2000-2001 | 6467 | 9363 | (-) 2896 | 66.07% |

| 2001-2002 | 5986 | 8540 | (-) 2554 | 70.09% |

Above Table indicates that during the first half of the eighties, export earnings could meet only 31% of the import bill which rose to 40% during the second half. Al through the nineties, the ratio in increasing upward and stood at 8.40% in 1997-98 and currently about 70%.

Top 10 Export Items of Bangladesh

Export Performance:

Despite narrow export base, supply-side-constraint and competitive world trading environment, Bangladesh’s export performance upto 2000-2001 has been quit impressive. But Export decreases during 2001-2002 due to global economic recession and 11 September attack.

Export Trend of Bangladesh

| FY | Export | Yearly | |

| 1990-1991 | 1717.6 | (+) 193.9 | (+) 12.72% |

| 1991-1992 | 1993.9 | (+) 276.3 | (+) 16.09% |

| 1992-1993 | 2382.9 | (+) 389.0 | (+) 19.51% |

| 1993-1994 | 2533.9 | (+) 151.0 | (+) 6.34% |

| 1994-1995 | 3472.6 | (+) 938.7 | (+) 37.04% |

| 1995-1996 | 3882.4 | (+) 409.8 | (+) 11.80% |

| 1996-1997 | 4418.3 | (+) 535.9 | (+) 13.80% |

| 1997-1998 | 5161.2 | (+) 742.9 | (+) 16.81% |

| 1998-1999 | 5313 | (+) 152.0 | (+) 2.93% |

| 1999-2000 | 5752 | (+) 439 | (+) 8.27% |

| 2001-2002 | 6467 | (+) 715 | (+) 12.43% |

| 2001-2002 | 5986 | (-) 481 | (-) 7.49% |

Export Composition:

As per current export list, the Bangladesh exports 125 products to world markets. however, the major 6 products contributing export accounting for around 90% of total exports.

Export Earnings by Major Commodities.

| 1999-2000 | 2000-2001 | 2001-2002 | 2002-2003 | |||||

| Value | % Share | Value | Value | % Share | % Share | Value | % Share | |

| Woven Garments | 3082.56 | 53.59% | 3363.90 | 2843.3 | 55.09% | 58.25% | 3258.27 | 49.76 |

| Knitwear | 1269.83 | 22.08% | 1496.22 | 940.3 | 18.22% | 25.90% | 1653.83 | 25.26 |

| Frozen Food | 343.82 | 5.98% | 363.22 | 293.8 | 5.69% | 6.28% | 321.81 | 4.91 |

| Jute Goods | 262.70 | 4.62% | 230.36 | 281.4 | 5.45% | 4.01% | 257.18 | 3.93 |

| Leather | 195.05 | 3.39% | 254.00 | 190.3 | 3.69% | 4.40% | 191.23 | 2.92 |

| Raw Jute | 71.62 | 1.25% | 67.18 | 107.8 | 2.09% | 1.16% | 82.46 | 1.26 |

| Total | 5171.58 | 90.91% | 5774.88 | 4656.9 | 87.23% | 100% | ||

Table shows that Woven Garments (52.20%) and Knitwear (24.38%), combinedly contributes (52.20+ 24.38) =76.58% to the total export earnings. We are excessively dependent on export of garments and Knitwear.

Export Markets:

Region-wise Export Markets

| Country / Region | 1972-73 | 1982-83 | 1992-93 | 1998-99 | 1999-2000 | 2000-2001 |

| American Region | 27.3% | 13.00% | 29.4% | 39.50% | 41.8% | 41.09% |

| EU Region | 26.4% | 18.6% | 29.8% | 46.36% | 44.5% | 45.78% |

| African Region | 12.6% | 13.1% | 6.7% | 1.05% | 0.7% | 0.53% |

| Asian Region | 7.5% | 27.7% | 18.3% | 7.68% | 7.5% | 7.17% |

| East European Region | 10.6% | 10.3% | 5.6% | 0.78% | 0.7% | 0.62% |

| Middle East Rgn. | 3.7% | 13.1% | 5.00% | 2.39% | 2.2% | 2.86% |

| Ocean Region | 2.6% | 2.2% | 1.5% | 0.77% | 0.8% | 0.45% |

| Others | 9.3% | 2.00% | 3.7% | 1.47% | 1.8% | 1.5% |

EU is the largest export destination of Bangladesh. American region is the 2nd largest market. Sharp fall of exports to the African, Asian and East European region points, as we are to export only traditional items. We should try to export diversified products to this region.

Industrialization of Agriculture

Trade position between Bangladesh and other BIMSTEC countries

Bangladesh and India:

| Year | Export | Import | Balance |

| 1995-96 | 72.47 | 1102.45 | (-) 1029.98 |

| 1996-97 | 46.25 | 921.73 | (-) 875.48 |

| 1997-98 | 65.58 | 935.62 | (-) 870.04 |

| 1998-99 | 59.79 | 1231.61 | (-) 1172.14 |

| 1999-2000 | 64.86 | 870.00 | (-) 805.14 |

| 2000-01 | 62.28 | 1174.41 | (-) 1112.13 |

| 2001-02 | 50.28 | 1018.80 | (-) 968.52 |

Bangladesh and Myanmar:

| Year | Export | Import | Balance |

| 1995-96 | 1.97 | 1.85 | (+) 0.12 |

| 1996-97 | 3.48 | 3.78 | (+) 0.30 |

| 1997-98 | 1.39 | 8.56 | (-) 7.17 |

| 1998-99 | 1.27 | 15.47 | (-) 14.20 |

| 1999-00 | 5.99 | 15.12 | (-) 9.13 |

| 2000-01 | 0.77 | 13.39 | (-) 12.62 |

| 2001-02 | 2.38 | 16.90 | (-) 14.52 |

Bangladesh and Thailand:

| Year | Export | Import | Balance |

| 1995-96 | 17.02 | 64.42 | (-) 47.40 |

| 1996-97 | 12.05 | 78.76 | (-) 66.71 |

| 1997-98 | 16.51 | 107.24 | (-) 90.73 |

| 1998-99 | 40.85 | 134.56 | (-) 93.71 |

| 1999-00 | 45.37 | 140.00 | (-) 94.63 |

| 2000-01 | 29.30 | 199.90 | (-) 170.06 |

| 2001-02 | 21.58 | 158.90 | (-) 137.32 |

Bangladesh and Sri Lanka:

| Year | Export | Import | Balance |

| 1995-96 | 3.27 | 10.44 | (-) 7.17 |

| 1996-97 | 2.40 | 12.16 | (-) 9.76 |

| 1997-98 | 1.25 | 4.39 | (-) 3.14 |

| 1998-99 | 3.54 | 7.23 | (-) 3.69 |

| 1999-00 | 4.76 | 7.20 | (-) 2.44 |

| 2000-01 | 2.62 | 8.06 | (-) 5.44 |

| 2001-02 | 2.07 | 6.10 | (-) 4.03 |

Bangladesh has significant trade relationship with other members of the BIMST-EC. Bangladesh, India and Sri Lanka are members of SAARC, SAPTA and the Bangkok Agreement. Bangladesh has a border trade agreement with Myanmar and a joint economic commission with Thailand. India is the largest trading partner. Bangladesh accounting for a total trade volume worth US $ 1 billion. However, despite geographic proximity and a more or less similar consumer behaviors (tastes and preferences), the BIMST-EC region is yet to emerge as a remarkable trading location for Bangladesh. Currently, Bangladesh’s exports to the BIMST-EC region are about 1.27% of her total exports and imports around 14% of total imports.

Bangladesh has been suffering from adverse trade balance with the member states of BIMST-EC. Bangladesh’s trade deficit with the other BIMST-EC countries increased form US$ 712 million in 1994-1995 to US$ 1124 million in 2001-2002. The rate of growth is around 58%. During the period, Bangladesh’s exports to the region increased from US$ 70 million to US$ 76 million, the rate of growth is over 8%.

To improve the Bangladesh economy and reduce the trade gap gradually, special preferential treatment under BIMST-EC should be provided to Bangladesh.

Tea Garden in Bangladesh

Major exportable products from Bangladesh to BIMST-EC countries

| Sl. | Product Name | India | Myanmar | Sri Lanka | Thailand |

| 1. | Frozen Food | 3 | – | – | 3 |

| 2. | Agri – Products | 3 | – | – | 3 |

| 3. | Tea | 3 | – | – | – |

| 4. | Chemical Products | 3 | 3 | 3 | 3 |

| 5. | Leather | 3 | 3 | 3 | 3 |

| 6. | Raw Jute | 3 | – | 3 | 3 |

| 7. | Jute Goods | 3 | 3 | 3 | 3 |

| 8. | Knitwear | 3 | – | – | 3 |

| 9. | Woven Garments | 3 | – | 3 | 3 |

Major importable products into Bangladesh from BIMST-EC countries

| Sl. | Product Name | India | Myanmar | Sri Lanka | Thailand |

| 1. | Live Animals & Animal Products | 3 | – | 3 | – |

| 2. | Frozen Foods | 3 | – | 3 | 3 |

| 3. | Agri Products | 3 | – | 3 | – |

| 4. | Mineral Products | 3 | – | 3 | 3 |

| 5. | Textiles | 3 | – | 3 | 3 |

| 6. | Metal, Motors, Vehicles and Machinery | 3 | – | 3 | 3 |

| 7. | Optical & Medical Instruments, Clock and Musical Instruments | 3 | – | 3 | 3 |

| 8. | Ceramics, Glassware, Stone, Cement | 3 | – | 3 | 3 |

| 9. | Hide Skins, Leather Footwear, Umbrella and gift items | 3 | – | 3 | 3 |

| 10. | Plastic & Rubber Products | 3 | – | 3 | 3 |

| 11. | Chemical and Cosmetics | 3 | – | 3 | 3 |

Commodity wise Bangladesh Export to BIMST-EC Countries

Value in ‘000’ US $ (1999-2000 & 2001-2002)

| Sl. | Product Name | India | Myanmar | Sri Lanka | Thailand | ||||

| 99-00 | 01-02 | 99-00 | 01-02 | 99-00 | 01-02 | 99-00 | 01-02 | ||

| 1. | Frozen Food | 6147 | 5298 | – | – | – | – | 22782 | 8336 |

| 2. | Agri – Products | 7 | 494 | – | – | – | – | 1 | – |

| 3. | Tea | 725 | 46 | – | – | – | – | – | 111 |

| 4. | Chemical Products | 14118 | 16202 | 449 | 2044 | 269 | 426 | 8007 | 9214 |

| 5. | Leather | 1353 | 812 | 86 | – | 12 | – | 311 | 325 |

| 6. | Raw Jute | 21069 | 14949 | – | – | 202 | – | 10921 | 760 |

| 7. | Jute Goods | 13098 | 2411 | 25 | – | 3949 | 1134 | 399 | 641 |

| 8. | Knitwear | 13 | 407 | – | 39 | – | 17 | 88 | 122 |

| 9. | Woven Garments | 1038 | 600 | – | – | 91 | 60 | 85 | 215 |

| 10. | Others | 7313 | 9061 | 42 | 299 | 132 | 432 | 2650 | 1852 |

| 11. | Total | 64881 | 50280 | 602 | 2382 | 4655 | 2069 | 45244 | 21576 |

Developing Bangladesh

Customs and Import Regimes

Customs and Import regimes in Bangladesh have, over the last decade, have been gradually simplified and liberalized. Significant relaxation has been achieved in import control procedures and policies. Pre-Shipment Inspections (PSI) has been introduced to ensure correct assessment of custom valuation of imported or exported goods.

Tariff structure has been remarkably liberalized and rationalized since the early nineties. The maximum tariff rate has been reduced to 32.5%. Number of operative tariff rates has also been brought down to five (including the zero rate). The Import-weighted average tariff rate has fallen to about 16%.

Duties and taxes payable by an importer in addition to customs duties include value added tax, supplementary duty on some products, infrastructure development surcharge at the rate 3.5%, advance income tax at the rate of 3% (adjustable with actually payable income tax).

Bangladesh and SAPTA

3rd Round of trade negotiations under the South Asian Preferential Trading Arrangement (SAPTA) have produced a considerable exchange of tariff concessions among the seven member states of SAARC, viz: Pakistan, India, Bangladesh, Nepal, Sri Lanka, Maldives and Bhutan. As an LDC, Bangladesh within the framework of non-reciprocity of SAPTA, has also offered modest concessions to the member states. However, Bangladesh could not enhance its export volume due to tariff, para tariff and a non-tariff barrier. Member countries did not allow Bangladeshi products to have desired market access, which has caused trade imbalances.

Besides trade, the SAPTA experience of Bangladesh is also not pleasant in respect of investment and technical cooperation. SAPTA regime needs to be improved further for the greater interest of the region.

BIMST-EC

- Bangladesh has tremendous potential for expansion of its export markets in the region specially in India (North and Northeastern region), Myanmar, Thailand and Sri Lanka provided that Tariff, Non-Tariff and para–Tariff barriers are removed or reduced at the requisite levels.

- The negative list approach is the most effective means by which Bangladesh can hope to expand its export markets in the region, since the positive list approach has failed so far to break through the present deadlock of market expansions for Bangladeshi products in the region.

- Bangladesh and Myanmar the two LDC’s should be accorded special and more favorable differential treatment among others in matters related to schedules of reduction commitments. LDCs should be given three years extended time period to meet their reduction commitments.

- Bangladesh should be allowed to impose a general revenue compensatory tariff over and above the agreed regional tariff.

Rules of origin

Rules of origin measures should be administered in a transparent and business friendly manner and should not be used as trade restrictive measure.

SAPTA rules of origin may be adopted for the BIMST-EC region also.

BIMST-EC should adopt transparent and harmonized rules among others on the following:

Simplification and harmonization of customs clearance procedures, harmonization of H.S. coding system, simplification and harmonization of import licensing procedures, simplification of banking facilities for import financing, custom cooperation & transit facilities. Transparent consultation and effective dispute settlement mechanism.

Visa exemption facility should be introduced eventually.

Air link should be established among the BIMST-EC Countries.

To prepare a common strategy for Foreign Direct Investment (FDI) and Joint Venture Investment in the following areas :

- Infrastructure

- Energy

- Tourism

- Setting up of export-oriented industries

- Textile

- Tele Communication

- Computer Software Development and Data Entry

- Leather and Leather Goods

- Light Industries

- Provision for common Gas and Electricity greed.

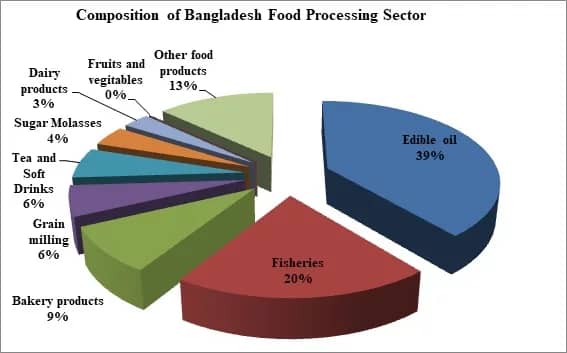

Composition of Bangladesh Food Processing Sector

In a recent study it was shown that there is considerable scope of expanding intra-trade among BIMSTEC countries in the following:

- Exports of Other woven textile fabrics (654) from Bangladesh to Thailand.

- Exports of Special textile fabrics, products (657) from Bangladesh to India and Thailand.

- Exports of Silk (261) from India to Bangladesh;

- Exports of Textile clothing accessories (847) from India to Thailand and Bangladesh;

- Exports of Synthetic fibre (266) from Thailand to India and Bangladesh;

- Exports of Manmade fibre (267) from Thailand to Bangladesh and India.

Policy makers and stakeholders in the textile/clothing industry in the exporting countries need to look at ways to translate this potential into larger trade flows.

6) For the longer term, the study shows that strong trade complementarities are emerging in the following areas:

- Exports of textiles from Bangladesh to India.

- Exports of textiles from Bangladesh to Thailand.

- Exports of clothing from India and Thailand;

- Exports of clothing from India and India;

- Exports of clothing from India and Sri Lanka;

- Exports of textiles from Sri Lanka to Thailand;

- Exports of Clothing from Bangladesh to Thailand

- Exports of textiles form Thailand to India;

- Exports of clothing from Thailand to Bangladesh;

- Exports of clothing from Sri Lanka to Thailand.

BIMSTEC framework can be used to set up exchange of information on best practices and also for encouraging the transfer of technology and investment among BIMSTEC members.

BIMSTEC Chamber should take initiative to create awareness about BIMSTEC among the Business people from all circles in order to strengthen the spirit of BIMSTEC cooperation and to elevate BIMSTEC profile in International fora.

Although one-fifth of the world population live in South Asian countries, they hold an insignificant position in the global economy accounting for only 1.9% of global GNP. Poverty is pervasive, bulk of the people below poverty line are in this region. Out region’s share in global trade is only 0.96% of export and 1.3% of import. The trade within the region is hardly 4.9% of our global trade and our countries rely heavily on the industrial economies for both import and export. The low volume of trade among SAARC countries means that the multiplier effects get their way to other countries, denying the region the benefits of higher production and employment. Therefore, BIMST-EC countries need to take initiative intensively to promote trade and investment to increase GDP growth.

In spite of failure of Cancun Negotiations, BIMSTE-EC should work closely together to formulate a common position in areas to be addressed in the forthcoming discussions of the new WTO Round. Areas of mutual interest may incorporate issues such as Agriculture, Transparency in Government procurement, Trade facilitation, Investment, Competition policy, Environment, Intellectual Property Rights, and Electronic Commerce which is a fast-moving issue and will have far and wide implications for all BIMST-EC countries. BIMST-EC should also work closely with the business sector to accelerate the development of regulatory framework for the use of electronic commerce so that BIMST-EC will be prepared as a group in such discussions at the WTO meetings.

I strongly feel that the BIMST-EC countries should take a collective stand and work together as a unified powerhouse in facing the challenges of the WTO system on the basis of Doha Development Round.

0 Comments